Your daily spending habits play a major role in building your credit score. Every bill you pay on time, every credit card swipe you manage responsibly, and every EMI you clear contribute to your financial profile. In today’s world, where lenders, banks, and even some employers look at creditworthiness, maintaining a healthy credit score has become more important than ever.

A strong credit score not only improves your chances of getting approved for loans but also helps you access better interest rates, higher limits, and faster approvals through a trusted loan application platform.

Why is Your Credit Score So Important Today?

A credit score is a reflection of your financial discipline. It’s beyond just a number. It tells lenders how responsibly you manage borrowed money and daily financial commitments.

Whether you are applying for a credit card, using loan apps, or planning to take a larger financial step in the future, your score matters because it affects:

- Loan approval chances

- Interest rates offered by lenders

- Credit card eligibility

- EMI options on purchases

- Access to better financial products

- Faster approvals through digital lending platforms

These days, many people rely on a loan application for urgent financial needs. However, without a good credit score, approvals may become difficult or expensive.

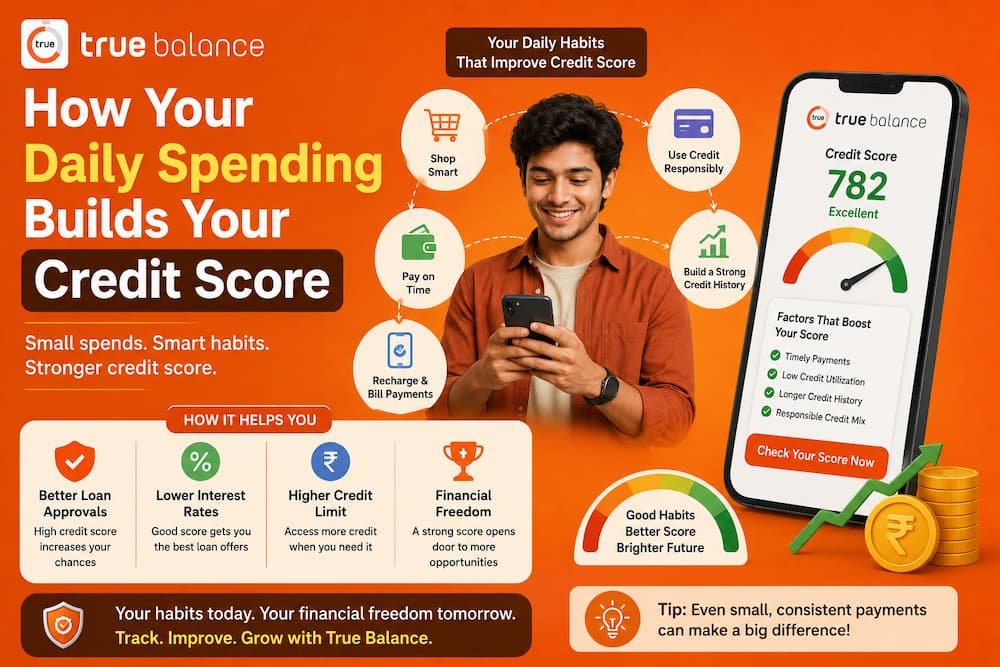

How Daily Spending Habits Affect Your Credit Score

While you may not think about it, your everyday financial choices directly shape your credit profile. Even small spending decisions can influence your score over time. Here’s how:

1. Paying Bills on Time Builds Trust

Your payment history plays a crucial role in determining your credit score, as it reflects how consistently and responsibly you repay your financial obligations. This includes:

- Credit card bill payments

- Utility bills

- Loan EMIs

- Subscription payments linked to credit cards

Repeatedly missing payments signals financial instability, while timely payments show responsibility. A simple habit like setting auto-pay reminders can significantly improve your credit profile over time.

2. Responsible Credit Card Usage Matters

Using a credit card wisely can strengthen your score. However, overspending can negatively impact it. For example:

- If your card limit is ₹1 lakh and you spend ₹90,000 regularly, lenders may see it as risky.

- Using around 20-30% of your limit is considered healthier.

Smart spending patterns show lenders that you can manage credit without depending heavily on it. So, that’s the key!

How Digital Payments and Loan Apps Have Changed Credit Behaviour

Digital finance has made borrowing and spending easier than ever. Many people use a credit loan app during emergencies or short-term financial gaps. While these platforms offer convenience, responsible usage is extremely important.

1. Borrow Only What You Need

Taking multiple loans frequently can negatively affect your score. Lenders may assume you are financially overdependent on borrowing.

Instead:

- Borrow only when necessary

- Repay EMIs on time

- Avoid applying for too many loans together

- Track repayment schedules carefully

Using a fast loan app responsibly can actually help build a positive repayment history.

2. Spending Discipline Creates Financial Opportunities

A good credit score is not built overnight. It is the result of consistent financial habits followed every single day.

Strong credit behaviour helps you:

- Qualify for higher loan amounts

- Access lower interest rates

- Get pre-approved offers

- Enjoy smoother financial planning

- Build long-term financial confidence

Whether you are planning to buy a home, start a business, or manage emergencies, your spending habits today shape your financial future tomorrow.

Common Spending Mistakes That Can Hurt Your Credit Score

Many people unknowingly make small financial mistakes that can gradually lower their credit score over time. This can be really frustrating. Mentioned below are some mistakes that can easily be avoided:

- Frequently Missing Due Dates: Even one delayed payment can impact your score and stay on your credit history for years.

- Maxing Out Credit Cards: Using your entire credit limit regularly creates a negative impression.

- Applying for Multiple Loans Together: Too many loan enquiries in a short period can reduce your score temporarily.

- Ignoring Small EMIs: People often prioritise bigger payments while forgetting smaller EMIs or bills, but every payment matters.

Smart Daily Habits That Improve Credit Score

If you are wondering how to genuinely improve your credit score, the answer lies in building consistent and responsible financial habits over time. It can be done simply by:

- Tracking your monthly expenses

- Paying bills before due dates

- Maintaining a budget

- Avoiding unnecessary debt

- Using credit responsibly

- Check your credit report regularly

- Keep older credit accounts active when possible

Wrapping Up

Your daily spending habits are far more powerful than they seem. Every timely payment, responsible purchase, and smart borrowing decision contributes toward building a stronger credit score. In a world where financial credibility matters for almost every major life decision, maintaining a healthy score can open doors to better opportunities, smoother approvals, and greater financial confidence.

If you are looking for a reliable loan application that combines convenience with transparency, True Balance stands out. From interest rates starting at 1% per month to a completely digital application process, the platform is designed to make borrowing smooth and hassle-free. Available on both Android and iOS, it offers flexible repayment options, foreclosure facilities, and loan amounts of up to ₹5 lakh through RBI-registered NBFCs/bank partners.

Download the True Balance Android or iOS loan app and experience a smarter way to borrow money.

Next Read: